Everyone dreams of having a home they can call their own. However, buying a home is not a piece of cake, especially with the soaring prices of houses. Going from paycheck to paycheck makes it challenging to acquire a property. But does that mean you have to give up on your dreams of buying your own house? The answer is no.

Getting a home loan can help you buy your first home. Not just that, you also get an array of benefits when you take a home loan. Want to know what they are or how to get approved for a home loan? You have stumbled upon the right article.

How to get approved for a home loan?

Applying for a home loan can be intimidating, especially if you have no guidance on how to get approval. This article will help you get an idea of how to get approval for a home loan. Here are three steps to getting a home loan.

- Get pre-approval: It is the first and crucial step of getting a loan. Your preferred lender will do a preliminary mortgage pre-approval which assesses your ability to get a home loan. The best part about this stage is that it tells what your budget should be, and you can look for homes accordingly. Additionally, pre-approval allows you to make an offer on a home and increases your credibility in front of sellers. You will get pre-approval letters which expire after a certain point. Therefore, you must keep updating the letter.

- Submit a complete application: Getting preapproved takes you a step closer to your dream house, and it implies that the lender is willing to give you a home loan. At this stage, You for other lenders and select the at this stage one with the lowest mortgage rates.

- Final approval from an underwriter: This is the last and final stage of getting a home loan. A professional underwriter will now skim through all your documents to identify any and all loopholes. They will also inspect the property. if you want to speed up the process, you must give your full cooperation at this point and solve all queries the underwriter may have.

While these three steps are essential in getting a home loan, some elements take center stage when getting pre-approval.

What is the lender looking for while approving a home loan?

Your lender wants to know that you can pay back the loan on time and with interest, so they want to know about your financial status. Here are four things any lender will check before approving your home loan.

- Employment history and income capacity: A part of your earnings will be required to pay the EMIs. Therefore the lender will check your previous and current employment status along with your monthly/yearly income.

- Credit score or credit history: It is, again, an essential factor that helps you get approval. The lender will check your previous credit history, including how well you have paid off previous EMIs. A good credit score will help you get approval faster. You can maintain a decent score by paying EMIs on time for any existing loans.

- Monthly debt: The lender will also check if you have any ongoing loans and their respective interest rates. This will include all types of loans, including student and car loans.

- Ability to give a down payment: When buying a home, you want to provide a down payment from your end. Usually, there is a specified percentage that you must pay. However, if you give a higher down payment, you will likely get approved.

Do not shy away from taking a home loan. Besides helping you buy your dream house, a home loan can benefit you in several other ways.

What are the benefits of getting a home loan?

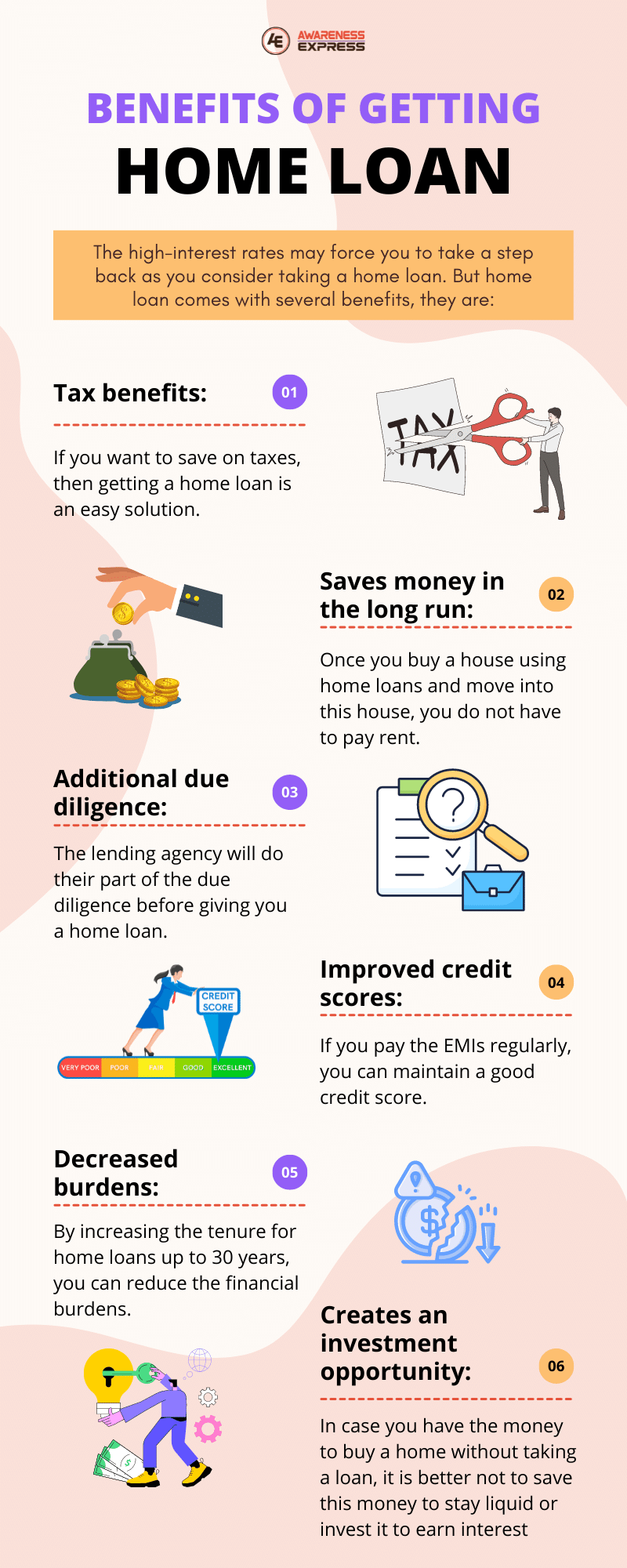

The high-interest rates may force you to take a step back as you consider taking a home loan. But home loans come with several benefits that are highlighted in this article.

- Tax benefits: If you want to save on taxes then getting a home loan is an easy solution. Those with home loans can enjoy tax benefits and can claim deductions.

- Saves money in the long run: Once you buy a house using home loans and move into this house, you do not have to pay rent. Although you are paying interest on the loan, at the end of the term, you will have a place to call your own.

- Additional due diligence: While you do your bit of homework while buying a property, the lending agency will also do their part of the due diligence before giving you a home loan. Hence, they will thoroughly check the house for you.

- Improved credit scores: If you pay the EMIs regularly, you can maintain a good credit score which will help you get a second home loan in the future. You can also easily get other types of loans like educational or car loans.

- Decreased burdens: Tenure for home loans can be extended up to 30 years. Therefore, you can repay the loan over a long period without taking on added financial burdens.

- Creates an investment opportunity: Now, this sounds weird, but home loans can create an investment opportunity. If you have the money to buy a home without taking a loan, it is better not to use it. You can save this money to stay liquid or invest it to earn interest while you take a home loan to buy your dream home.

Final words:

Buying a house is a major achievement and a huge financial decision. Therefore, it is imperative that before you commit, you know every minute detail of your loan and read the fine print to avoid all confusion. You must also remember that to keep the financial burden under check; you should only borrow the amount you need and not the amount that is available.

{kind=link}